Global Unicorn Index 2026

The Hurun Research Institute today released the Global Unicorn Index 2026, a ranking of the world’s unicorns, defined as start-ups founded in the 2000s, worth at least a billion dollars and not yet listed on a public exchange. The cut-off was 1 January 2026, with significant changes in valuation updated up to the date of publication. Hurun Research Institute has been tracking unicorns since 2017.

GLOBAL UNICORN INDEX 2026

IN SEARCH OF START-UPS FOUNDED AFTER 2000, WITH A VALUATION OF US$1BN AND NOT YET LISTED ON A PUBLIC EXCHANGE.

HURUN RESEARCH INSTITUTE FINDS RECORD 1603 UNICORNS IN THE WORLD, UP 5.3% OR 80 UNICORNS.

TOTAL VALUE OF UNICORNS IN WORLD US$8TN, UP STAGGERING 43% ON BACK OF AI

308 UNICORNS NEWLY MINTED, NEARLY ONE EVERY DAY OF PAST YEAR. 139 ‘PROMOTED’ AND 88 ‘DEMOTED’ FROM LAST YEAR’S INDEX.

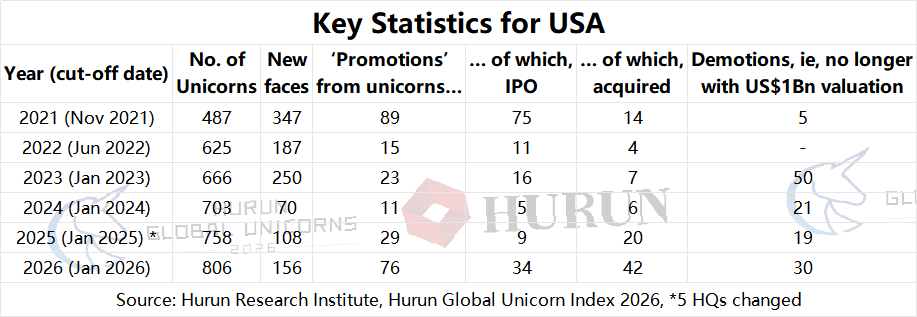

USA LED WITH 806 UNICORNS, UP 48, ACCOUNTING FOR 50.3% OF WORLD TOTAL. 156 NEW ENTRIES, ONE UNICORN MINTED IN THE US EVERY TWO DAYS.

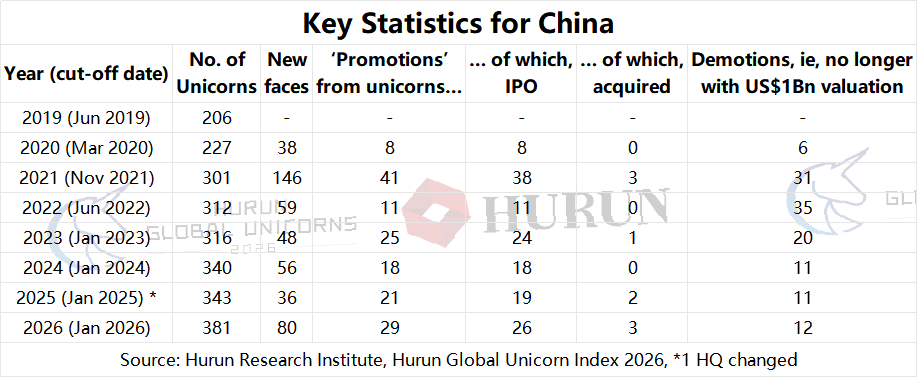

CHINA SECOND WITH 381, UP 38, AND WITH 80 UNICORNS MINTED IN YEAR. ONE NEW UNCORN MINTED EVERY FIVE DAYS, MUCH FASTER THAN LAST YEAR’S ONE NEW UNICORN EVERY TEN DAYS. THE US AND CHINA HAVE 74% OF WORLD’S UNICORNS BETWEEN THEM.

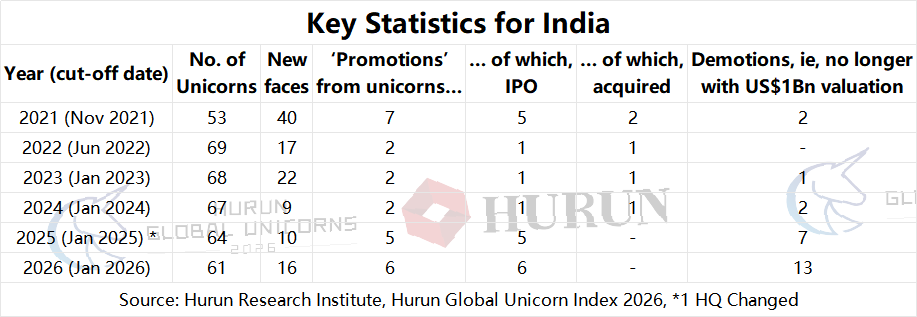

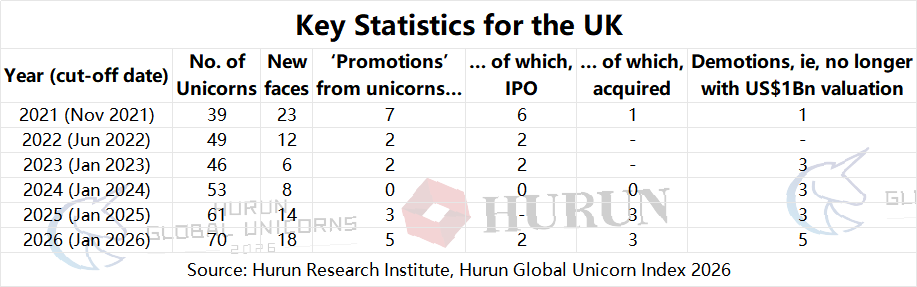

UK, WITH 70 UNICORNS, UP 9 OVERTOOK INDIA FOR THIRD PLACE WITH 61 UNICORNS.

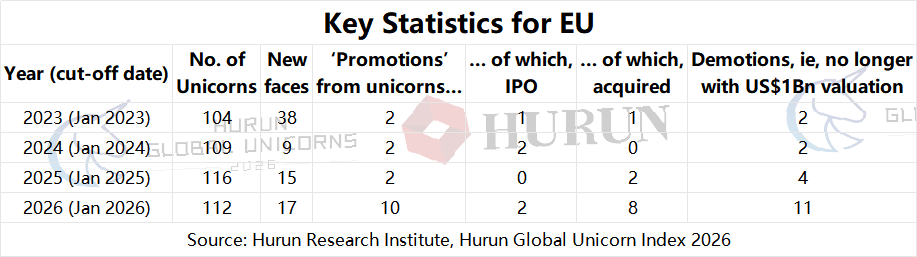

EU COUNTRIES 112 UNICORNS, DOWN 4.

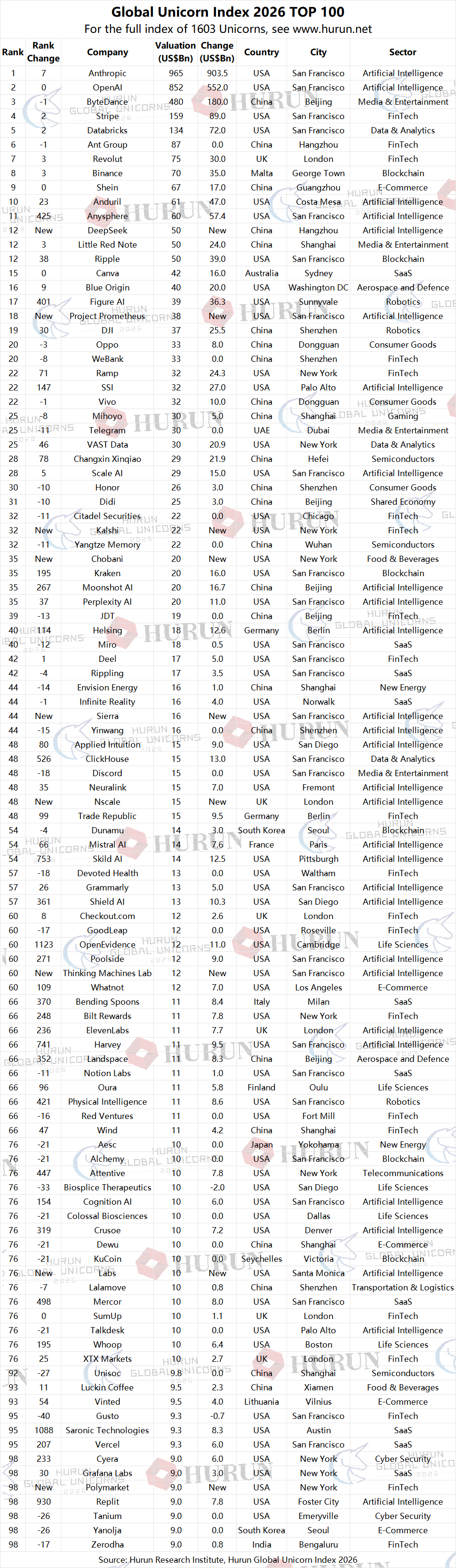

YEAR OF AI. CLAUDE OWNER ANTHROPIC ROCKETS UP TO BECOME MOST VALUABLE UNICORN IN WORLD, NOW WORTH US$965BN, UP US$904BN — THE SINGLE LARGEST ONE-YEAR VALUATION GAIN EVER RECORDED.

CHATGPT OWNER OPENAI SECOND AT US$852BN, ADDING US$552BN.

TIKTOK AND DOUBAO AI ASSISTANT OWNER BYTEDANCE, DOWN TO 3RD PLACE, DESPITE VALUATION UP US$180BN TO US$480BN

5 UNICORNS, UP 1, WORTH MORE THAN US$100BN.

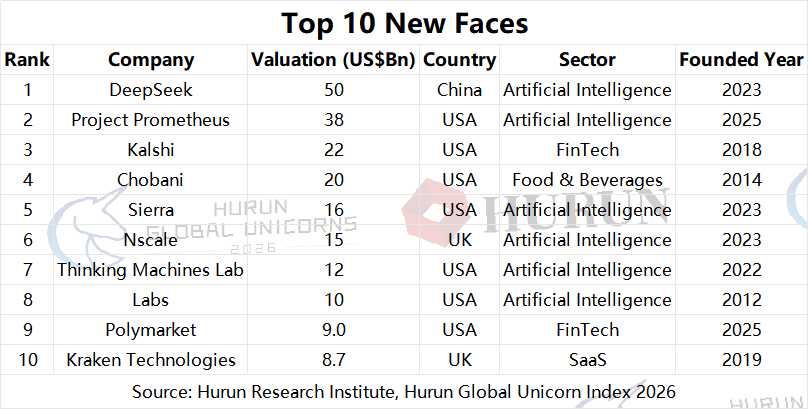

HANGZHOU-BASED AI ASSISTANT DEEPSEEK HIGHEST NEW ENTRY, BREAKING STRAIGHT INTO TOP 15 WITH VALUE OF US$50BN.

91 UNICORNS, UP 27, WORTH US$10BN OR MORE.

CRYPTO EXCHANGE GIANT BINANCE DOUBLES, ADDING US$35BN TO REACH US$70BN AND ENTERED THE TOP 10.

LIFE SCIENCES AND DEFENCE HAVE GOOD YEARS WITH US-BASED MEDICAL AI PLATFORM OPENEVIDENCE, AND US-BASED DEFENCE TECH SARONIC TECHNOLOGIES, BOTH RISING OVER 1000 PLACES TO TOP 100

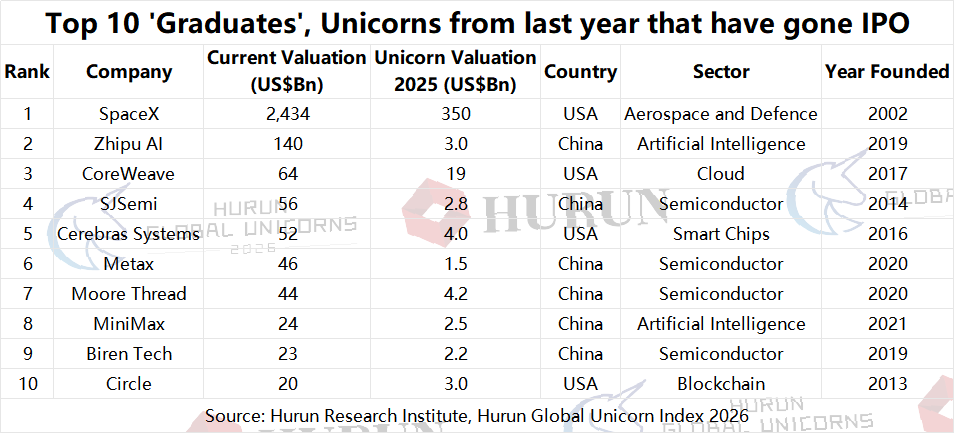

139 UNICORNS FROM LAST YEAR ‘PROMOTED’ OUT OF THE INDEX THIS YEAR, OF WHICH 75 IPO (34 FROM US, 26 FROM CHINA AND 15 FROM ‘REST OF WORLD’) AND 64 MERGED/ACQUIRED. BIGGEST ‘GRADUATE’ FROM LAST YEAR’S UNICORNS IS SPACEX, NOW WORTH OVER US$2TN, A SIX-FOLD LEAP FROM ITS US$350BN BASELINE LAST YEAR.

AI LEADS WITH 36% OF UNICORNS VALUE, AHEAD OF FINTECH WITH 13%. BY UNICORN NUMBERS, FINTECH LEADS WITH 216 UNICORNS, FOLLOWED BY AI WITH 215 AND SAAS WITH 181. TOP THREE SECTORS MADE UP 38% OF UNICORNS.

US UNICORNS IN AI, SAAS, LIFE SCIENCES, FINTECH; CHINA UNICORNS SEMICONDUCTORS, AI AND NEW ENERGY, WHILST ‘REST OF WORLD’ FINTECH, E-COMMERCE, SAAS AND BLOCKCHAIN.

POLAND, BANGLADESH AND IRAN REMAIN THE LARGEST ECONOMIES WITHOUT A UNICORN.

SAN FRANCISCO WORLD’S UNICORN CAPITAL WITH 222 UNICORNS, UP 23, FOLLOWED BY NEW YORK WITH 141, AND BEIJING WITH 86.

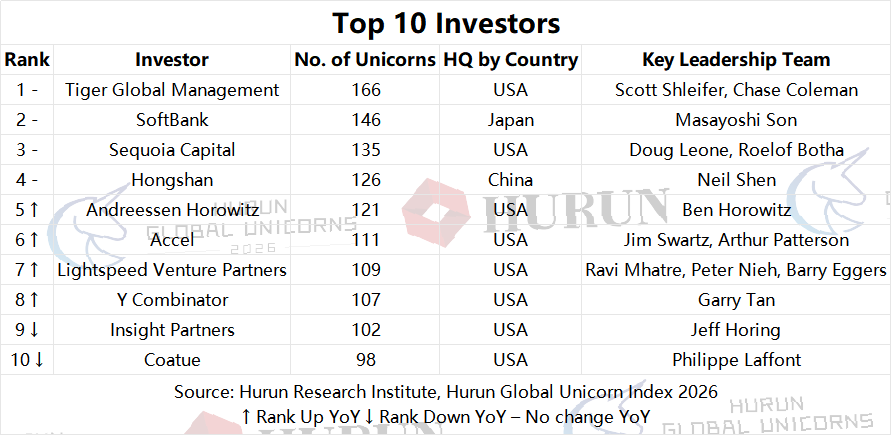

TIGER GLOBAL IS THE WORLD'S MOST PROLIFIC UNICORN INVESTOR WITH 166 INVESTMENTS, FOLLOWED BY SOFTBANK AT 146.

AVERAGE AGE OF UNICORN IS 10.3YRS. AVERAGE AGE OF UNICORN FOUNDERS AT TIME OF FOUNDING 35YRS

(25 June 2026, Guangzhou, Mumbai, and London) The Hurun Research Institute today released the Global Unicorn Index 2026, a ranking of the world’s unicorns, defined as start-ups founded in the 2000s, worth at least a billion dollars and not yet listed on a public exchange. The cut-off was 1 January 2026, with significant changes in valuation updated up to the date of publication. Hurun Research Institute has been tracking unicorns since 2017. This is the eighth year of the Global Unicorn Index.

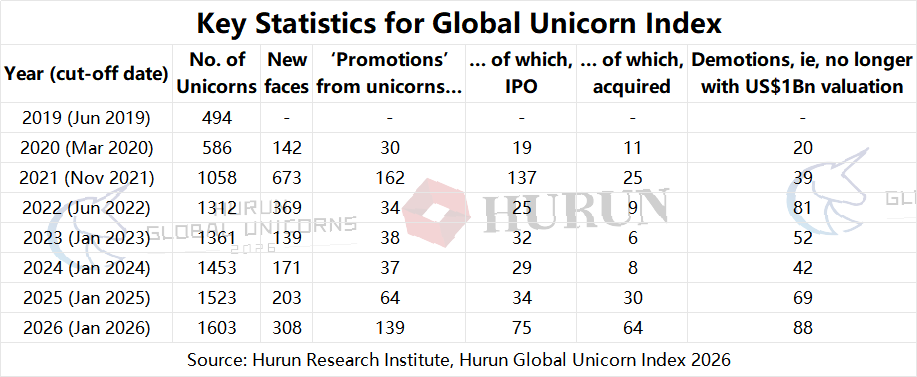

Hurun Research Institute found 1603 unicorns in the world, based in 52 countries and 299 cities. 610 unicorns saw their valuations rise, of which 308 were new faces. 178 saw their valuations drop, of which 88 were ‘demoted’ as their valuation no longer made the US$1bn cut. 139 were ‘promoted’ out of the list, of which 75 went IPO and 64 were merged/acquired. 903 saw no change to their valuations.

The world’s unicorns are disrupting financial services, business management solutions and healthcare. 74% sell software and services, led by FinTech, SaaS, and AI, whilst 26% have a physical product, led by Semiconductors, New Energy, Biotech, and HealthTech.

Hurun Chairman and Chief Researcher Rupert Hoogewerf said:

"With SpaceX officially graduating to the public markets as a history-making titan, the global unicorn landscape has officially crowned a new order. Anthropic and OpenAI now command the absolute peak of the index, representing an unprecedented concentration of private AI capital as they go for trillion-dollar valuations. This AI era is witnessing the world's next generation of mega-corporations being forged in record time."

"In 2026, AI has moved from theme to engine. Anthropic's leap from eighth to first place globally — adding nearly US$1Tn in a single year — is the most dramatic valuation rise we have ever recorded across eight years of this index. It signals that the race to build the most capable and trusted AI system is now the defining competition in the global economy."

"The total value of the world's unicorns has surged 43% to US$8Tn, driven almost entirely by the AI boom. The Top 10 alone are worth US$3.9Tn — nearly half the entire list. This concentration of economic value is unprecedented and reflects investor conviction that AI will produce a small number of extraordinarily valuable companies."

"308 unicorns were newly minted this year — nearly one every day — up from 203 last year. This is still short of the 2021 peak of 700, but the quality of this year's cohort is higher: many new entrants in AI, Robotics and New Energy came in at multi-billion-dollar valuations from day one."

"DeepSeek, entering the Top 15 as a brand-new entrant at US$50Bn, is a landmark. Founded in Hangzhou, it is proof that China's AI ecosystem is producing frontier models capable of competing globally — and doing so with far less compute than Western rivals. It raises profound questions about where the real moat in AI ultimately lies."

“The sectors that performed best were AI, FinTech, SaaS, Robotics and Life Sciences. Others of note included Aerospace and Defence, New Energy, Semiconductors, Blockchain and Cyber Security.”

"FinTech and AI currently boast 216 and 215 unicorns respectively, sharing the crown as the world's leading unicorn sectors, but AI unicorns are now officially worth triple FinTech unicorns. The centre of gravity is shifting from E-Commerce platforms eight years ago to FinTech transactions and now to AI platforms."

"SaaS remains a durable contributor with 181 unicorns, but the fastest-growing sub-segment within SaaS is now AI-native software — products built from the ground up on large language models. Many of this year's new SaaS entrants are effectively AI companies wearing a different label."

"Life Sciences has quietly grown to 152 unicorns, reflecting sustained investor interest in the intersection of AI and biology. Companies like OpenEvidence, Oura and Whoop are examples of how AI is transforming diagnostics, drug discovery, and personal health monitoring."

"Robotics is having its moment. Figure AI entering at US$39Bn and Physical Intelligence at US$11Bn, signal that the humanoid and autonomous robotics sector is transitioning from lab to ledger. We expect this to become one of the defining sectors of the next decade."

"The USA has 806 unicorns — 50.3% of the world's total. California alone is home to 427 unicorns valued at approximately US$3.6Tn. The Bay Area's dominance in AI and frontier technology is not merely maintained — it is widening."

"China's unicorn count grew to 381, up 38, driven by 80 new entrants including DeepSeek, 3D printer Bambu Lab, and a wave of semiconductor companies. 26 Chinese unicorns went public this year — second highest country — reflecting a maturing ecosystem where IPO windows are opening even in a challenging macro environment."

"Indians co-founded 217 unicorns --- 156 are abroad, led by 142 in the USA, and 61 on home soil — together valued at US$599Bn. From Perplexity AI and Anysphere to Zerodha and Razorpay, Indian founders are simultaneously building the world's AI stack, pioneering global fintech, and transforming one of its largest domestic economies. India is not simply producing entrepreneurs; it is producing the architects of the global economy."

"Revolut at US$75Bn confirms that London remains a world-class FinTech hub. The UK's 70 unicorns include standouts in AI, New Energy, and FinTech. Nscale, entering at US$15Bn, is a sign that European AI infrastructure is beginning to scale."

"Tiger Global Management holds the crown as the world's most prolific unicorn investor with 166 investments, ahead of SoftBank with 146 and Sequoia Capital with 135. The composition of the top investor list has shifted decisively toward AI-focused funds over the past three years."

"75 unicorns graduated to public markets this year, more than double last year's 34. USA led with 34 IPOs followed by China with 26. The biggest was Elon Musk’s SpaceX (now worth over US$2Tn). Other successful US ‘unicorn grads’ included CoreWeave (US$64Bn), Figma (US$12Bn) and Chime (US$7Bn). This suggests that after several years of suppression, the IPO window is cautiously reopening. China’s big IPOs are mostly in AI, led by Zhipu AI (now worth US$140Bn), MiniMax (US$24Bn) and semiconductor plays SJSemi (US$56Bn), Moore Thread (US$46Bn), Metax (US$45Bn), Biren Tech (US$23Bn), and Axera (US$2.1Bn), as well as EV platform Voyah (US$2.3Bn), robotics firm Geek+ (US$2.6Bn), and enterprise software players Pateo (US$4Bn) and Manycore (US$3.2Bn)— a cohort that reflects the full breadth of China’s technology ecosystem.”

"88 unicorns were shut down or marked below US$1bn — a sobering reminder that not all high valuations endure. The clean-out is healthy: it redirects talent and capital toward companies with stronger fundamentals."

"Defence technology is emerging as a new unicorn powerhouse. Anduril has risen to 10th globally, quadrupling to US$61Bn, Helsing from Germany at US$18Bn and Shield AI has entered at US$13Bn. Geopolitical tensions are concentrating venture capital into AI-enabled defence systems at an accelerating pace."

"San Francisco now has 222 unicorns — extending its lead as the world's unicorn capital. Within China, Beijing continues to lead, followed by Shanghai. Shenzhen was third, reflecting southern China's growing strength in hardware, semiconductors and AI-enabled manufacturing. Hangzhou, home to DeepSeek and Moonshot AI, added 3 to reach 25. Guangzhou, home to fast-fashion platform Shein, was up one to 24. Together, these five cities account for two-thirds of the national total — a concentration that underscores how tightly China’s startup ecosystem clusters around a handful of innovation hubs.”

“19 companies founded in the past year have already achieved unicorn status — more than one a month in the very year they were founded. This is the AI era compression effect: what once took a decade now takes months. But speed alone does not explain it. Two trends stand out: one is Serial Founders, who have the trust of investors, and second is Founder Factories, those with senior positions in big companies like OpenAI and Google, who then branch out on their own."

“The most powerful ‘Founder Factory’ in the world today is San Francisco-based OpenAI. Former VP of Research Dario Amodei left to build Anthropic, now the world’s most valuable unicorn. Former Chief Scientist Ilya Sutskever departed to found SSI, valued at US$32Bn. Former CTO Mira Murati launched Thinking Machines Lab, valued at US$12Bn. In total, OpenAI alumni have spawned unicorns collectively worth over US$1Tn — an astonishing legacy from a single institution. Google has similarly seeded the ecosystem: former Google DeepMind and Google Brain researchers co-founded several AI unicorns, including Nobel laureate Demis Hassabis who founded London-based AI drug discovery startup Isomorphic Labs. The pattern is clear: the best founder factories is tacit, hands-on experience with frontier-scale computing.”

“Serial Founders are increasingly a defining feature of the unicorn landscape. Jeff Bezos now has two unicorns in the Top 50: Blue Origin at US$40Bn (ranked 16th) and Project Prometheus at US$38Bn (ranked 18th). Even after SpaceX, Elon Musk still retains three unicorns: OpenAI, in which he is a co-founder, Neuralink at US$15Bn, and The Boring Company at US$7Bn. Two others including Shanghai-based founder Zhang Lei, as well as Joe Lonsdale also have three.”

“The next wave of unicorns is forming in technologies that most people have barely heard of yet. Quantum computing is represented by PsiQuantum (US$7Bn, USA) and SandboxAQ (US$5.6Bn, USA), both working to commercialise quantum advantage within this decade. In fusion energy, Helion Energy (US$5.4Bn) and Commonwealth Fusion (US$4Bn) are racing to deliver commercially viable fusion power. Nuclear fission is making a private-sector comeback with TerraPower (US$3.8Bn), Valar Atomics (US$2Bn), and France’s Newcleo (US$1.7Bn). Neurotech is represented by Elon Musk’s Neuralink (US$15Bn), working on brain-computer interfaces. In Hydrogen, Chinese startups including Spiche and Dongyue Future Hydrogen are building out the supply chain. These sectors are pre-revenue or pre-commercial today, but history suggests that the unicorns of tomorrow are precisely the companies that look implausible today.”

“A decade ago, the concept of a billion-dollar startup was remarkable enough to coin a new word: unicorn. Today, a trillion-dollar private company is no longer a fantasy — Anthropic and OpenAI are both within touching distance. We also expect the total number of unicorns to surpass 2000 within three years, driven by AI, robotics, and clean energy. IPO volumes should continue to recover: from 34 last year to 75 this year, and we expect 100 or more in 2027 as windows in the US, UK, and India remain open. The average unicorn will be younger and more capital-efficient than at any point in the history of this index. The defining feature of the next decade will not be how many unicorns exist, but how fast they reach the trillion-dollar mark — and how many of them stay there.”

“There is a lot of money to be made if you get into these unicorns early enough. In the US, SpaceX has gone up 6-fold and Cloud computing platform CoreWeave has tripled. Big money has been made in China, led by AI and semiconductor plays. Beijing’s Zhipu AI has achieved a scarcely believable 43x in just one year, whilst SJSemi was up 20x, Metax 30x, Moore Thread and Biren Tech each up 10x.”

“The world’s top unicorn investors generated exceptional exit returns in the year to January 2026. Sequoia Capital and SoftBank were among the major beneficiaries of the Klarna IPO, which valued the Swedish fintech at approximately US$15Bn at listing — a remarkable recovery from its 2022 write-down. Coatue, which backed CoreWeave (now valued at US$64Bn in public markets), and Andreessen Horowitz, an early Figma backer ahead of its public listing, both achieved landmark exits. These exits matter beyond the returns themselves: every successful unicorn IPO validates the model, recycles capital into the next cohort of founders, and deepens the talent pool as employees become angels and founders. The virtuous cycle of venture capital is accelerating, and the top ten investors are at its centre.”

“The 2025–2026 venture capital landscape is defined by extreme bifurcation, with capital intensely concentrated at the top through massive AI mega-rounds—such as SoftBank and a16z’s participation in OpenAI’s $122Bn round, and Coatue backing Anthropic’s $30Bn raise—alongside high-conviction defence tech investments like Founders Fund’s $2.5Bn bet on Anduril. Meanwhile, growth crossover investors like Tiger Global face a tightening environment, recently compounded by a landmark January 2026 Indian Supreme Court ruling that disrupted Mauritius-based offshore tax exemptions and heavily complicated exit economics in emerging markets. Consequently, the liquidity landscape has shifted away from the traditional IPO frenzy toward strategic corporate M&A and secondary markets, where buyers now wield increased pricing power and compress valuation multiples despite globally robust exit volumes.”

“M&A is the other side of the unicorn story that rarely gets told. This year, 64 unicorns were acquired or merged — and the motivations split into two distinct categories. The first is defensive: large incumbents acquiring unicorns to neutralise a competitive threat before it matures. Google’s US$32Bn acquisition of Wiz is the clearest example — a cloud security company that had grown fast enough to challenge existing enterprise relationships. ServiceNow’s acquisition of Moveworks (US$2.1Bn), Snowflake’s acquisition of dbt Labs (US$4.2Bn), and Cisco’s absorption of Chronosphere (US$1.6Bn) all follow the same logic: buy the disruptor before the disruption arrives. The second motivation is integrative: incumbents acquiring unicorns to embed their technology into the core product. Microsoft’s deep partnership with OpenAI is the defining example of this era — less an acquisition than a co-creation, with Microsoft weaving OpenAI’s models into Azure, Office, and Bing. ADP’s acquisition of Paradox AI (US$1.5Bn) and Empower Retirement’s acquisition of Guideline (US$1.2Bn) reflect the same integrative ambition in HR and financial services. The message for founders is clear: build something that threatens a giant, and the exit will find you.”

"We have updated our 'unicorn zoo'. There are now 5 Thunderbirds — startups worth US$100bn or more — up from 4 last year, and 91 Griffins — startups worth US$10bn or more — up by 27. Combined with our pipeline animals, the ladder now runs: Cheetahs → Gazelles → Unicorns → Griffins → Thunderbirds. We are thinking of adding in a mythological animal to represent a trillion-dollar unicorn, a Leviathan, the massive primordial seas monster. SpaceX was the first Leviathan, just before its IPO."

Stock Markets and Currencies.

Major stock indices generally performed remarkably well in the year to the 1 January 2026 cut-off. In the USA, the tech-heavy Nasdaq rose by 19%, while the S&P 500 locked in a 15% gain. European markets mirrored this strong trajectory: London’s FTSE 100 Index rose by 18%, the Paris-based Euronext 100 was up 15%, and both Germany’s DAX and the EURO STOXX 50 climbed 13%. In Asian markets, Shenzhen was up 40%, Hong Kong's Hang Seng Index staged a strong recovery to post an 33% increase and Shanghai was up 27%. India's Sensex also maintained a steady positive momentum, rising 6%.

Over the same period, the US Dollar demonstrated broad weakness against a majority of global currencies. The greenback fell 11.5% against the Euro, 7% against the British Pound, 4.2% against the Chinese Yuan and was stable against the Japanese Yen. Against the Indian Rupee, the dollar gained 5%.

Alternative and commodity markets told a nuanced story. Bitcoin began and ended the year near the same level — around US$93,000— representing a near-flat full-year return of under 1%, despite hitting an intra-year all-time high of approximately $126,000 in October before halving in value at the time of the release of this index. The traditional energy market was far from stable: West Texas Intermediate (WTI) crude oil declined by approximately 16–20% over the year, weighed down by oversupply and weak demand as OPEC+ unwound production cuts.

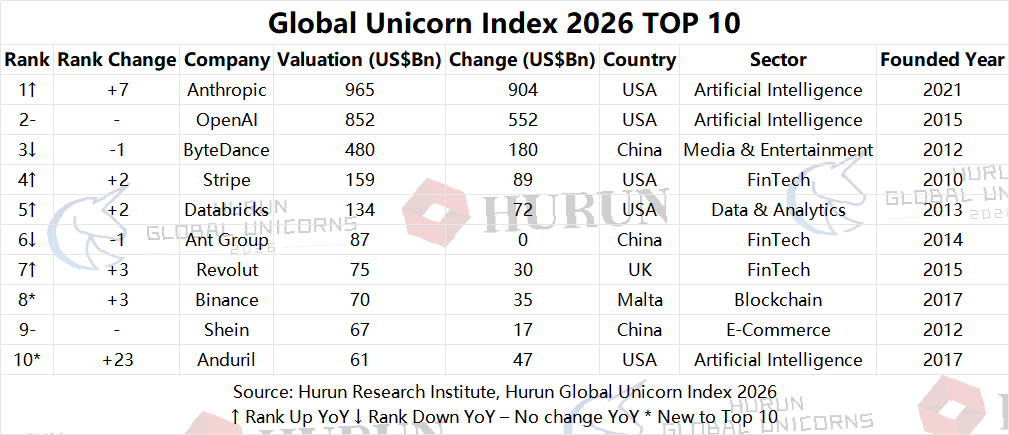

Top 10 Unicorns in the World

The AI Super-Surge: Anthropic rocketed up 7 positions into the #1 spot globally, adding an astronomical US$904Bn to reach a US$965Bn valuation. OpenAI maintained its position as the second most valuable unicorn globally. The firm saw its valuation more than double, growing by US$552Bn to achieve a current valuation of US$852Bn. Consequently, former frontrunner ByteDance dropped one position to #3, sitting at US$480Bn despite a US$180Bn gain.

The cut-off to enter the top tier rose drastically to US$61Bn, an increase of US$16Bn compared to last year. Binance officially entered the Top 10 for the first time at #8, doubling its valuation by adding US$35Bn to reach US$70Bn. Fast-growing fintech Revolut also climbed three places to #7 with a valuation of US$75Bn, while fast-fashion giant Shein takes the #9 with US$67Bn. Defence tech Anduril made a massive leap of 23 positions to break into the elite group at #10 with a valuation of US$61Bn.

Geographically, USA companies now tighten their grip on the elite board, claiming 5 of the Top 10 spots (Anthropic, OpenAI, Stripe, Databricks, and Anduril). China accounts for 3 entries (ByteDance, Ant Group, and Shein), while the UK (Revolut) and Malta (Binance) hold 1 spot each.

Table 1: Global Unicorn Index 2026 TOP 10

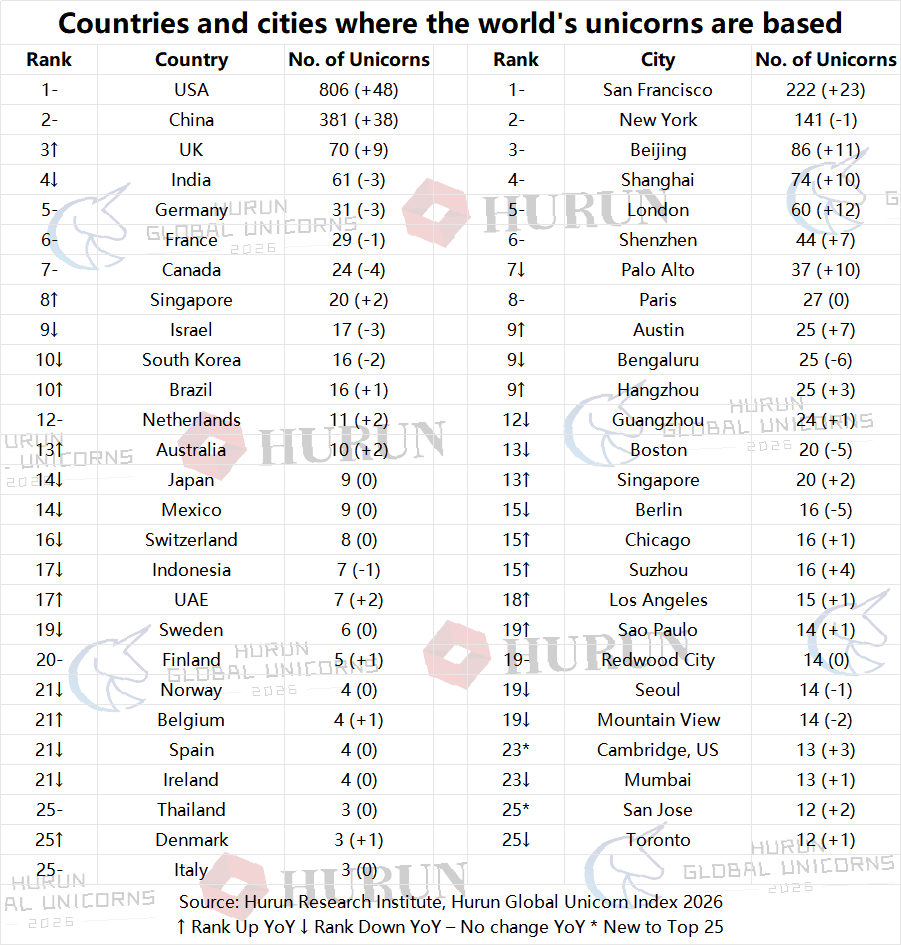

Where are the World’s Unicorns based?

The world’s unicorns come from 52 countries, an increase of 117% from 2019, spread around 299 cities, an increase of 153% from 2019, and down from 307 from last year.

The USA led the world with 806 unicorns (adding 48), followed by China with 381 (adding 38). The UK overtook India for third place. Singapore overtook Israel and South Korea for 8th place.

The fastest growing city for unicorns was San Francisco, adding 23 in one year, followed by London, Beijing, Palo Alto, Shanghai and Austin.

By city, San Francisco retained the title of ‘World Unicorn Capital’ with 222 unicorns (gaining 23), followed by New York with 141. In China, the top unicorn strongholds are Beijing with 86, Shanghai with 74, Shenzhen with 44, Hangzhou with 25, and Guangzhou with 24. In Europe, London leads with 60, followed by Paris with 27, and Berlin with 16. In India, Bengaluru led with 25, followed by Mumbai with 13. In Asia, outside of China, Singapore led with 20 ahead of Seoul with 14.

Table 2: Countries and cities where the world’s unicorns are based

Key countries

USA: The USA continues to set the pace for global startup innovation with a record 806 unicorns — half of the world's total — adding 156 new faces in the past year alone. Valuations surged, led by Anthropic at US$965Bn, and OpenAI at US$852Bn.

Leading in SaaS, FinTech, AI, and Life Sciences, US unicorns are also gaining pace in frontier sectors including humanoid robotics Figure AI (US$39Bn), quantum tech (PsiQuantum US$7Bn, SandboxAQ US$5.6Bn), fusion energy (Helion Energy US$5.4Bn, Commonwealth Fusion US$4Bn), and genetic engineering (Colossal Biosciences US$10Bn).

Project Prometheus (US$38Bn, Jeff Bezos' physical AI lab), Kalshi (US$22Bn, prediction markets), Chobani (US$20Bn, food & beverages), Sierra (US$16Bn, enterprise AI), Thinking Machines Lab (US$12Bn, ex-OpenAI CTO Mira Murati) are notable new entrants.

China: China was second with 381 unicorns, up 38. China had 26 IPOs of unicorns from last year’s index. In the last six years, China's unicorns have risen from 227 to 381. Leading entrants: Beijing-based Media & Entertainment giant ByteDance (US$480Bn), Hangzhou-based FinTech platform Ant Group (US$87Bn), Guangzhou-based E-Commerce retailer Shein (US$67Bn), and Hangzhou-based Artificial Intelligence new entrant DeepSeek (US$50Bn).

ByteDance grew US$180Bn to a valuation of US$480Bn, deepening its impact through AI assistant Doubao. Little Red Note added US$24Bn to reach US$50Bn. Moonshot AI (US$20Bn, +US$16.7Bn) was the standout LLM story alongside StepFun (US$6Bn, +US$3.8Bn).

UK: The UK boasts 70 unicorns worth US$295Bn, led by Revolut (US$75Bn, up US$30Bn). Notable new entrants: Nscale (US$15Bn, AI infrastructure, including data centers, partnered with Microsoft, Nvidia & OpenAI for Stargate UK), Kraken Technologies (US$8.7Bn, energy operating system spun out of Octopus Energy), Wayve (US$8.6Bn, autonomous vehicles). FinTech dominates at US$158Bn, followed by Artificial Intelligence (US$42Bn) and SaaS (US$14Bn). 1 IPO this year, but the UK remains a top global tech and finance hub.

India: India ranks fourth with 61 unicorns, led by broking startup Zerodha (US$9Bn), e-commerce Zepto (US$7Bn) and payments infrastructure company, Razorpay (US$6Bn). With 6 IPOs this year, the ecosystem shows strong momentum and growing global relevance.

Indians co-founded a further 156 unicorns outside India — over 90% in the US, with 4 in the UK and 2 in Singapore and 1 in Germany. This diaspora impact makes India one of the world's most influential startup talent exporters.

The European Union now hosts 112 unicorns, reflecting a dynamic year with 17 new additions, 2 IPOs, 8 mergers and acquisitions, and 9 drop-offs. The EU was led by Germany with 31 unicorns, driven by strengths in Fintech, SaaS, and AI, followed by France with 29, supported by strong public-private AI and deep tech initiatives led by Mistral AI (US$14Bn). The Netherlands has 11 unicorns, Sweden contributed 6, and Finland 5 — notably home to Oura (US$11Bn), the world's highest-value Healthcare unicorn per employee. Other European contributors include Belgium, Spain, and Ireland with 4 unicorns each, while Denmark and Italy hold 3 each. Total EU unicorn value stands at US$415Bn, led by Binance (US$70Bn, Malta), Helsing (US$18Bn, Germany), Trade Republic (US$15Bn, Germany), and Mistral AI (US$14Bn, France).

Southeast Asia: The region's 35 unicorns are worth US$80bn collectively. Singapore (20) dominates, with FinTech accounting for nearly half of all regional unicorns. Indonesia follows with 7 entries (down by one), while Thailand holds steady at 3. The region faces consolidation pressure as 6 companies exited the index in 2026.

GCC: The Gulf grew from 7 to 9 unicorns in 2026, collectively valued at US$45Bn, led by UAE (7) and Saudi Arabia (2). Telegram (US$30Bn, UAE) towers over the rest. New entrants include two Gulf-based startups this year. Saudi Arabia's Tabby (US$4.5Bn, buy-now-pay-later) and Tamara (US$1Bn) signal the Kingdom's growing fintech ambition, while UAE-based Kitopi (US$1.6Bn, cloud kitchens) and AI.Tech (US$1.5bn) show diversification beyond finance.

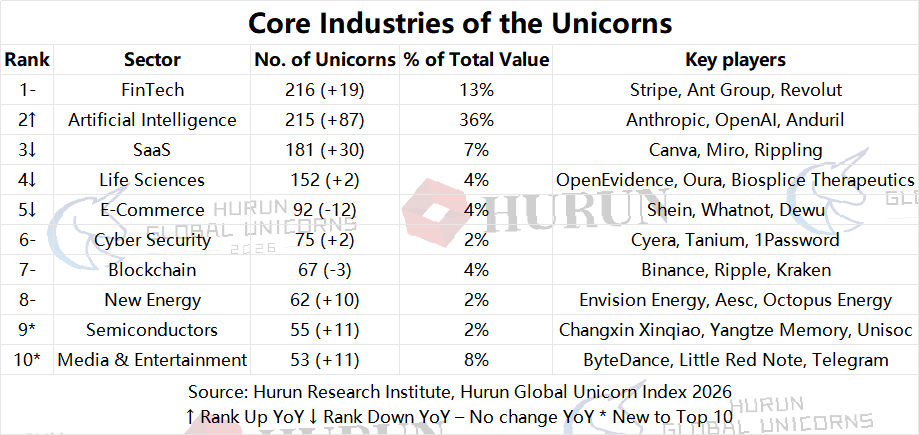

What industries do they come from?

8 years ago the unicorn story was about eCommerce. Then it switched to FinTech and today it is Artificial Intelligence that dominates.

Industries that have been most disrupted by unicorns in the past year were Financial Services, Business Management Solutions, Healthcare and Retail.

AI is the standout growth story of 2026 — with 215 unicorns, up a massive 87 in a single year, and accounting for 36% of total unicorn value; the highest share of any sector. Together with FinTech and SaaS, these three sectors account for roughly one-third of all unicorns. Leading firms like OpenAI, Anthropic, and Anduril are driving outsized valuations as AI embeds itself across enterprise and consumer platforms in both the US and China. In the AI space, the USA leads significantly with 132 unicorns, while China (47), the UK (9), Canada (5), and Germany (4) round out the top five countries. Key AI companies that successfully achieved IPOs include Zhipu AI, MiniMax, Mininglamp Tech, Fractal Analytics and Cidi.

With 216 unicorns — up 19 from last year — and commanding 13% of total unicorn value, FinTech retains its position as the world's largest startup sector. Dominated by the US, UK, China, and India, it spans digital lending, neobanks, payment gateways, and trading platforms, fundamentally reshaping how financial services are accessed globally. The FinTech sector is heavily dominated by the USA with 93 unicorns, followed by the UK (24), India (22), China (9), and Singapore (7). Notable companies in this space that have successfully gone public include Chime, Klarna, Webull, eToro, and Groww.

181 SaaS unicorns — up 30 on the year — power the backend of modern business with 7% of total unicorn value. From enterprise tools and productivity platforms to industry-specific solutions, these startups deliver recurring value at scale. While the US dominates, countries like Germany, Australia, and India are carving out strong niches in vertical SaaS. The SaaS industry is anchored by the USA with 120 unicorns, alongside China (20), France (6), Germany (6), UK, and Australia (4 each). Recent notable public listings in this sector feature Netskope, Manycore, and Pateo.

With 152 unicorns and 4% of total value, Life Sciences encompasses HealthTech and BioTech. The US remains dominant, but China and Europe are catching up fast. Innovations in telehealth, medical devices, diagnostics, gene therapy, and drug discovery signal a long-term investment trend with tangible real-world impact. The USA remains the strongest player in Life Sciences with 97 unicorns, followed by China (36), the UK (8), India (5), and France (2).

92 unicorns — down 12 — with 4% of total value, E-Commerce reflects a maturing sector undergoing consolidation. Giants in China and the USA drive the momentum, while emerging markets including India, Brazil, and Southeast Asia contribute to a broader retail revolution across fashion, groceries, and marketplace verticals. E-Commerce is tightly contested, led jointly by China and the USA with 22 unicorns each, and supported by India (11), France (6), Brazil and South Korea (5 each). Standout companies that have successfully listed include Lenskart, Meesho, Il Makiage, Navan, and Urban Company.

Amid escalating digital threats, 75 Cybersecurity unicorns — up 2 — represent 2% of total unicorn value. This mission-critical sector is led by the USA, with active ecosystems in Israel and Canada. Threat detection, identity protection, and cloud security are among the fastest-growing sub-sectors. The USA holds a massive lead in Cyber Security with 58 unicorns, outpacing Israel (6), Canada (5), Switzerland (1), and Lithuania (1).

67 Blockchain unicorns — down 3 — account for 4% of total value, with crypto exchanges leading on valuation. Binance heads the pack at US$70Bn, while London-based Blockchain.com saw its valuation halve to US$7Bn. Despite a count decline, value concentration among top exchanges keeps this sector's share elevated. Blockchain innovation is geographically widespread, topped by the USA with 37 unicorns, the UK (6), Canada (4), Seychelles (2), and Singapore (2). The sector saw successful IPOs from prominent players like Circle, Figure Technologies, BitGo, Gemini, and HashKey.

New Energy retains at rank 8, with 62 unicorns — up 10 — and 2% of total value. The sector's rise reflects surging investment in clean energy infrastructure globally. Companies are targeting solar, wind, energy storage, and grid technology as the world accelerates its transition away from fossil fuels. China is the undisputed leader in the New Energy sector with 35 unicorns, while the USA (18), the UK (3), France (2), and Japan (1) trail behind.

55 Semiconductor unicorns — a new entry to the Top 10 — represent 2% of total value. China dominates this category, driven by national ambitions for chip self-sufficiency, with companies designing mobile chipsets, memory, and custom silicon. The sector's rise reflects sustained global demand for AI-capable hardware amid ongoing geopolitical supply chain tensions. Driven by national self-sufficiency goals, China dominates the Semiconductor space with 48 unicorns, leaving the USA (5), Singapore (1), and Israel (1) far behind.

53 unicorns in Media & Entertainment — also a new entry — account for a notable 8% of total value, driven largely by ByteDance's outsized valuation. The sector encompasses short-form video, social content platforms, and messaging apps, with China and Europe well represented alongside the US. The Media & Entertainment industry is led by the USA with 23 unicorns and China with 11, followed by the UK (4), the UAE (3), and France (2). Triller stands out as the notable IPO in this sector.

Other Notable Sectors

The Robotics sector is scaling rapidly, featuring 50 unicorns that contribute a total combined valuation of US$175Bn. Leading the charge in this hardware-driven ecosystem are standout innovative players like Figure AI, DJI, and Physical Intelligence. China leads the Robotics ecosystem with 32 unicorns, while the USA (15), Singapore (1), France (1), and Germany (1) also feature in the top ranks. Geek+ is a notable public listing in this hardware-focused space.

Transportation & Logistics continues to be a crucial global industry, boasting 47 unicorns that hold a collective market value of US$115Bn. The sector is primarily anchored by high-impact mobility and delivery disruptors such as Lalamove, Gopuff, and Zipline International. The USA claims the top spot in Transportation & Logistics with 22 unicorns, followed by China (11), India (3), Germany (2), and Brazil (2).

Driven by massive frontier technology investments, the Aerospace and Defence sector commands a collective US$140Bn valuation across its 44 unicorns. With former sector titan SpaceX graduating to the public markets, the private ecosystem is now led by major innovators like Anduril, Jeff Bezos’ Blue Origin and Beijing-based Landspace. Aerospace & Defence is primarily driven by the USA with 23 unicorns and China with 14, while Germany (2) and India, Portugal, Finland, Australia, and France feature 1 Aerospace & Defence unicorn each.

Providing the essential backbone for the modern digital economy, the Cloud & Infrastructure sector includes 32 unicorns valued at US$65Bn. Standout enterprises driving networking and cloud computing advancements globally include DriveNets, EON, and Vultr. In Cloud & Infrastructure, the USA leads the pack with 23 unicorns, followed by China (5), UK (1), Israel (1), Finland (1), UK (1), and the Netherlands (1).

Capturing shifting retail and lifestyle trends, the Consumer Goods sector houses 31 unicorns that hold a combined valuation of US$142Bn. The landscape is predominantly shaped by digitally native and high-growth consumer apparel brands such as Vuori, Skims, and GP Club. The Consumer Goods sector is evenly led by China and the USA with 11 unicorns each, followed by the UK (3) and South Korea (2).

The Data & Analytics space remains vital for enterprise optimisation, featuring 30 unicorns that collectively represent US$234Bn in private value. Leading this data revolution are powerhouse analytics platforms and tech giants including Databricks, VAST Data, and ClickHouse. The Data & Analytics sector is overwhelmingly based in the USA with 24 unicorns, with minor representation from China (2), Norway (1), India (1), and Canada (1).

The Food & Beverages industry features 26 unicorns, demonstrating sustained consumer demand with a total valuation of US$72Bn. Market momentum in this space is heavily driven by prominent global brands and disruptors like Chobani, Luckin Coffee, and Genki Forest. China tops the Food & Beverages sector with 14 unicorns, while the USA (8), India (1), Chile (1), Indonesia (1), and Germany (1) make up the rest of the leading nations.

The Education sector continues its digital transformation journey, encompassing 21 unicorns with a collective market worth of US$43Bn. Key platforms revolutionising modern learning and corporate upskilling include Guild Education, Articulate, and Course Hero. Educational technology is spearheaded by the USA with 13 unicorns, followed by India (3), the UK (1), Australia (1) and Greece (1).

China has designated the ‘Low Altitude Economy’ — covering drones, eVTOL aircraft, unmanned logistics, and autonomous aerial systems — a national strategic priority. The Global Unicorn Index 2026 identifies 12 unicorns operating in the low altitude space, with a combined valuation of approximately US$60Bn. China accounts for 8 of these, reflecting the country’s dominance in drone manufacturing and commercialisation: DJI alone is valued at US$37Bn and ranks in the global Top 20. Other notable Chinese players include AVIC (drones, US$1.9Bn), Aerofugia (eVTOL, US$1.8Bn), Volant (eVTOL, US$1.5Bn), Tengden (drones, US$1.5Bn), and XAG (agricultural drones, US$1Bn). The USA contributes Skydio (US$4.4Bn, AI-powered drones) and Performance Drone (US$1.2Bn, military drones). The sector is expected to grow rapidly as China integrates low altitude corridors into its urban infrastructure, making it a material component of the unicorn index in the years ahead.

Real Estate Tech accounts for 19 unicorns, leveraging technology to modernise property markets and achieving a combined valuation of US$40Bn. Leading innovators disrupting property management and commercial real estate operations include JD Property, DNE, and Side. The Real Estate Tech market is heavily anchored in the USA with 15 unicorns, alongside China (2), South Korea (1), and India (1).

The Shared Economy sector retains a notable presence on the global index, with 17 unicorns contributing a total valuation of US$70Bn. Despite broader market consolidations, it continues to be led by major global mobility platforms like Didi, Bolt, and CloudKitchens. The Shared Economy sector is led by China with 6 unicorns and the USA with 4, followed by India (3), Estonia (1), and the UK (1). Notable successful exits in this category include public listings by Via Transportation and Caocao.

ClimateTech sector retains a growing presence on the global unicorn index, with 17 unicorns contributing a total valuation of US$24Bn. Reflecting the increasing global focus on sustainability, it continues to be led by major innovative platforms like 1Komma5, Solugen, and Gradiant. The ClimateTech sector is overwhelmingly led by the USA with 12 unicorns, followed by Germany (1), Switzerland (1), Japan (1), Canada (1), and the UK (1).

Table 3: Core Industries of the Unicorns

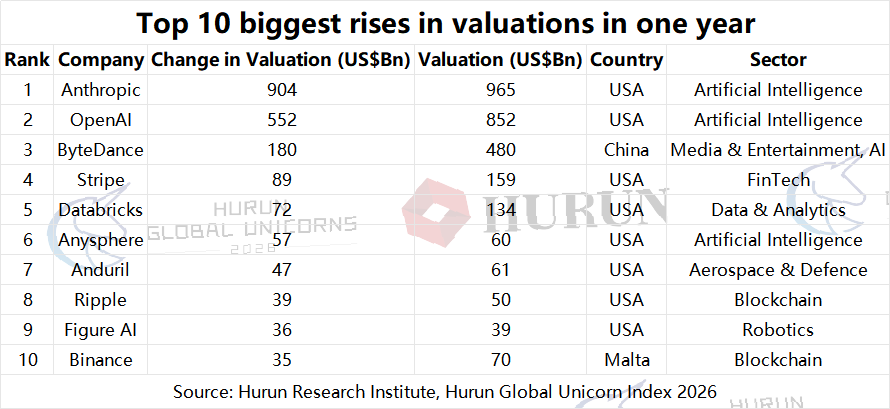

Who’s Up?

610 unicorns saw their valuation increase, of which 308 were new unicorns. The valuation increases and new unicorns came to US$3.6Tn, of which new unicorns made up US$724Bn.

The biggest jumps in valuation were Anthropic and OpenAI.

The new unicorns came from the US (156), China (80), and the Rest of the World (72), led by China-based DeepSeek, and US-based Project Prometheus. By city, San Francisco led with 48 new unicorns, followed by Beijing and NYC with 22 each, while London recorded 18, and Shanghai, Palo Alto, and Shenzhen followed with 18, 14, and 10.

Of the companies promoted from last year’s Global Unicorn List, the USA led with 76 promotions (34 IPOs and 42 mergers/acquisitions), while China followed with 29 promotions (26 IPOs and 3 acquisitions). You would have made a lot of money had you invested in any of these. SpaceX has gone up 6-fold, whilst Zhipu AI has achieved a scarcely believable 43x in just one year.

Of the new faces to this year’s index, two prediction market unicorns burst onto the scene: Kalshi (US$22Bn) and Polymarket (US$9Bn). One surprise in this age of AI was Chobani, which has popularised Greek yogurt and is now valued at US$20Bn.

Table 4: Top 10 biggest rises in valuations in one year

Table 5: Top 10 New Faces

Table 6: Top 10 ‘Graduates’, Unicorns from last year that have gone IPO

Youngest Unicorns

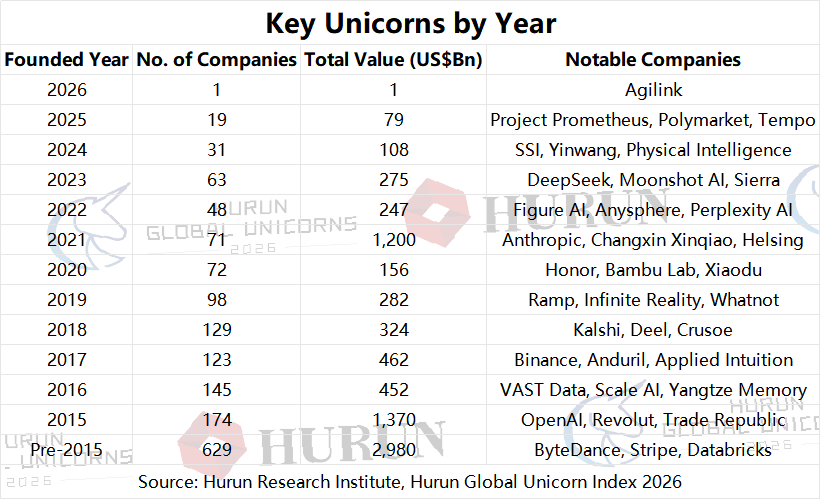

Around 50% of the unicorns in the Global Unicorn Index 2026 were founded in the last 10 years. Remarkably, 19 companies founded in 2025 have already achieved unicorn status — nearly one new unicorn per month in the year they were founded. The speed of AI-driven value creation continues to compress the timeline from founding to billion-dollar valuation.

Table 7: Key Unicorns by Year

Serial Entrepreneurs

One of the most compelling revelations from this year's Hurun Global Unicorn Index is the rise of serial entrepreneurs—visionary founders behind multiple billion-dollar ventures.

The number of founders with two unicorns surged by over 60% (from 33 to 53), proving that building multiple billion-dollar companies is increasingly becoming a replicable playbook rather than a rare anomaly. Five years ago, the concept of a 'repeat unicorn founder' was rare enough to be remarkable; today it is a recognised investment category in its own right.

Three have founded three unicorns still on the list: Elon Musk (OpenAI, Neuralink, The Boring Company), Shanghai-based Zhang Lei (Envision Energy, Aesc, Envision Digital) and Joe Lonsdale (Erebor, Addepar, Epirus). What makes Musk special is that he has two trillion-dollar erstwhile unicorns with SpaceX and Tesla.

Founder Factories

The most powerful ‘Founder Factory’ in the world today is San Francisco-based OpenAI. Dario Amodei and Daniela Amodei left OpenAI to build Anthropic, now the world’s most valuable unicorn. John Schulman, Barrett Zoph, Lilian Weng, and others co-founded the same venture. Former chief scientist Ilya Sutskever departed to found SSI, valued at US$32Bn. Former CTO Mira Murati launched Thinking Machines Lab, valued at US$12Bn. In total, OpenAI alumni have spawned unicorns collectively worth over US$1Tn — an astonishing legacy from a single institution. Google has similarly seeded the ecosystem: former Google DeepMind and Google Brain researchers co-founded several AI unicorns, including Nobel laureate Demis Hassabis who founded AI drug discovery startup Isomorphic Labs. Alibaba alumni have driven a wave of China’s AI and SaaS unicorns. For example, Misa Zhu, the former head of Alibaba's deep learning lab, founded the AR/AI glasses unicorn Rokid; Jerry Wang, Alibaba’s first cloud business chief, launched the massive AI+IoT platform Tuya Smart; and former Alibaba security executive Jiang Tao built the US$1.3Bn AI risk management SaaS, Tongdun Technology.

The pattern is clear: the best founder factories are today’s AI frontier labs, not business schools. Historically, elite MBA programs like Stanford GSB and Harvard Business School, alongside top consulting firms like McKinsey and investment bank Goldman Sachs, were the primary incubators for unicorn founders. Today, the core bottleneck to building a generational tech company is no longer generic business strategy or corporate networking — it is tacit, hands-on experience with frontier-scale computing.

Frontier labs provide their talent with "compute privilege," allowing researchers to solve unprecedented engineering and scaling bottlenecks that simply cannot be simulated in a classroom. When these researchers leave, they carry highly specialised technical moats and algorithmic secrets. Venture capitalists now heavily index on this rare technical pedigree, knowing that while a brilliant researcher can easily be surrounded by seasoned business operators, a seasoned business operator cannot fake frontier AI expertise. In the generative AI era, building the model is the business, making the research lab the ultimate launchpad.

Which investors are the best at finding Unicorns?

The world’s most prolific unicorn investors continue to wield extraordinary influence over the global startup economy. Please note, the full list of the top unicorn investors will come out in a separate press release.

Tiger Global Management holds the crown as the world's most prolific unicorn investor with 166 investments, leading SoftBank (146) in second place. Sequoia Capital follows in third place with 135 investments.

The composition of the Top 10 remains heavily anchored by US-based firms, with China's Hongshan the only non-US VC in the Top 10.

Together these ten institutions have backed over 1,300 unicorns — effectively co-authoring the modern global startup ecosystem. Their largest current positions include Anthropic, OpenAI, Stripe, Databricks, and Anduril. Key exits in the past year include Klarna (backed by Sequoia and SoftBank), CoreWeave (Coatue, Fidelity), Figma (Andreessen Horowitz, Sequoia), and Chime (Softbank, General Atlantic). Each major exit returns capital that is rapidly redeployed into the next generation of AI and deep tech founders.

Table 8: Top 10 Investors

Key Statistics

Table 9A: Key Statistics for Global Unicorn Index

Table 9B: Key Statistics for USA

Table 9C: Key Statistics for EU

Table 9D: Key Statistics for China

Table 9E: Key Statistics for India

Table 9F: Key Statistics for the UK

Methodology

The Global Unicorn Index is compiled by the Hurun Research Institute and includes unlisted companies founded in the 2000s with a current valuation of US$1Bn or more.

The cut-off for this year’s index was 1 January 2026, with significant valuation changes updated up to the date of release. SpaceX, for example, was a unicorn at the cut-off date, but has since graduated, so has been taken off the list.

Many of the world’s top investment houses provided details of their portfolio, which the Hurun Research team cross-checked against specialised investment databases, industry experts, media sources, as well as unicorn co-founders.

Valuing unicorns can be tricky. The very nature of these super-fast-growing companies makes valuations hard to pin down, but to ensure consistency of the valuations, Hurun Research used the most recent valuation based on a sizeable round. Where it becomes harder is when a unicorn is underperforming or on its way down, since founders and investors are mostly loath to want to announce a down-round. In this case, Hurun Research used industry comparatives to ascertain a new lower valuation.

Startups like US-based Signal are not on the Hurun Global Unicorns Index because they have not commercialised their platforms.

Unicorns leave the Hurun Global Unicorn Index either by being ‘promoted’, ie, by listing on a public exchange (IPO) or being acquired, or by being ‘demoted’, when their value drops below US$1Bn.

Hurun Research Institute has been tracking unicorns since 2017.

Hurun Disclaimer. All the data collection and the research have been carried out by Hurun Research. This report is meant for information purposes only. Reasonable care and caution have been taken in preparing this report. The information contained in this report has been obtained from sources that are considered reliable. By accessing and/or using any part of the report, the user accepts this disclaimer and exclusion of liability, which operates to the benefit of Hurun. Hurun does not guarantee the accuracy, adequacy, or completeness of any information contained in the report, and neither shall it be responsible for any errors or omissions in or for the results obtained from the use of such information. No third party whose information is referenced in this report under the credit assumes any liability towards the user with respect to its information. Hurun shall not be liable for any decisions made by the user based on this report (including those of investment or divestiture), and the user takes full responsibility for their decisions made based on this report. Hurun shall not be liable to any user of this report (and expressly disclaim liability) for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential losses, loss of profit, lost business and economic loss regardless of the cause or form of action and regardless of whether or not any such loss could have been foreseen.

About Hurun Inc.

Promoting Entrepreneurship Through Lists and Research

Oxford, Shanghai, Mumbai

Established in the United Kingdom in 1999, Hurun is a research and media group, promoting entrepreneurship through its lists and research. Widely regarded as an opinion-leader in the world of business, Hurun generated 8 billion views on the Hurun brand in 2025, mainly in China and India, and recently expanded to the UK, US, Canada, and Australia.

Best known for the Hurun Rich List series, telling the stories of the world’s successful entrepreneurs in China, India, and the world, Hurun’s other key series focus on young businesses and entrepreneurs, through the Hurun Unicorns Index and the Hurun Uth series.

Hurun has grown to become the world’s largest list compiler for start-ups, ranking over 3000 start-ups across the world through its annual Hurun Global Unicorns Index (startups with a valuation of US$1Bn+), and two Hurun Future Unicorn Indexes: Gazelles, most likely to ‘go unicorn’ within three years, and Cheetahs, most likely to ‘go unicorn’ within five years.

The Hurun Uth series includes the Under25s, Under30s, Under35s, and Under40s awards, representing the cream of each generation of young entrepreneurs who have founded businesses with a social impact and worth US$1m, US$10m, US$50m, and US$100m, respectively.

Other key IPs include the Hurun 500 series, ranking the most valuable companies in the world, China and India, the Hurun Global High Schools List, ranking the world’s best independent high schools, the Hurun Philanthropy List, ranking the biggest philanthropists and the Hurun Art List, ranking the world’s most successful artists alive today.

Hurun provides research reports co-branded with some of the world’s leading financial institutions and regional governments.

Hurun hosts high-profile events across China and India, as well as London, Paris, New York, LA, Toronto, Vancouver, Sydney, Luxembourg, Istanbul, Dubai, and Singapore.

For further information, see www.hurun.net.

For media inquiries, please contact:

Hurun Report

Porsha Pan

Mobile: +86-139 1838 7446

Email: porsha.pan@hurun.net

Global Unicorn Index 2026 TOP 100

Appendix

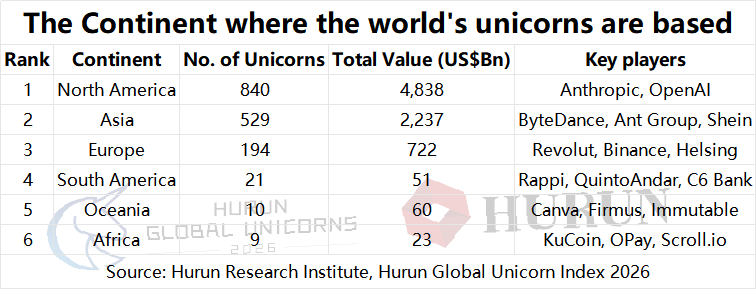

Appendix 1: The Continent where the world’s unicorns are based

Appendix 2: Unicorns founded by Indians outside of India

Table: Unicorns outside of India with an Indian co-founder

Appendix 3: Unicorns founded by Chinese outside of China

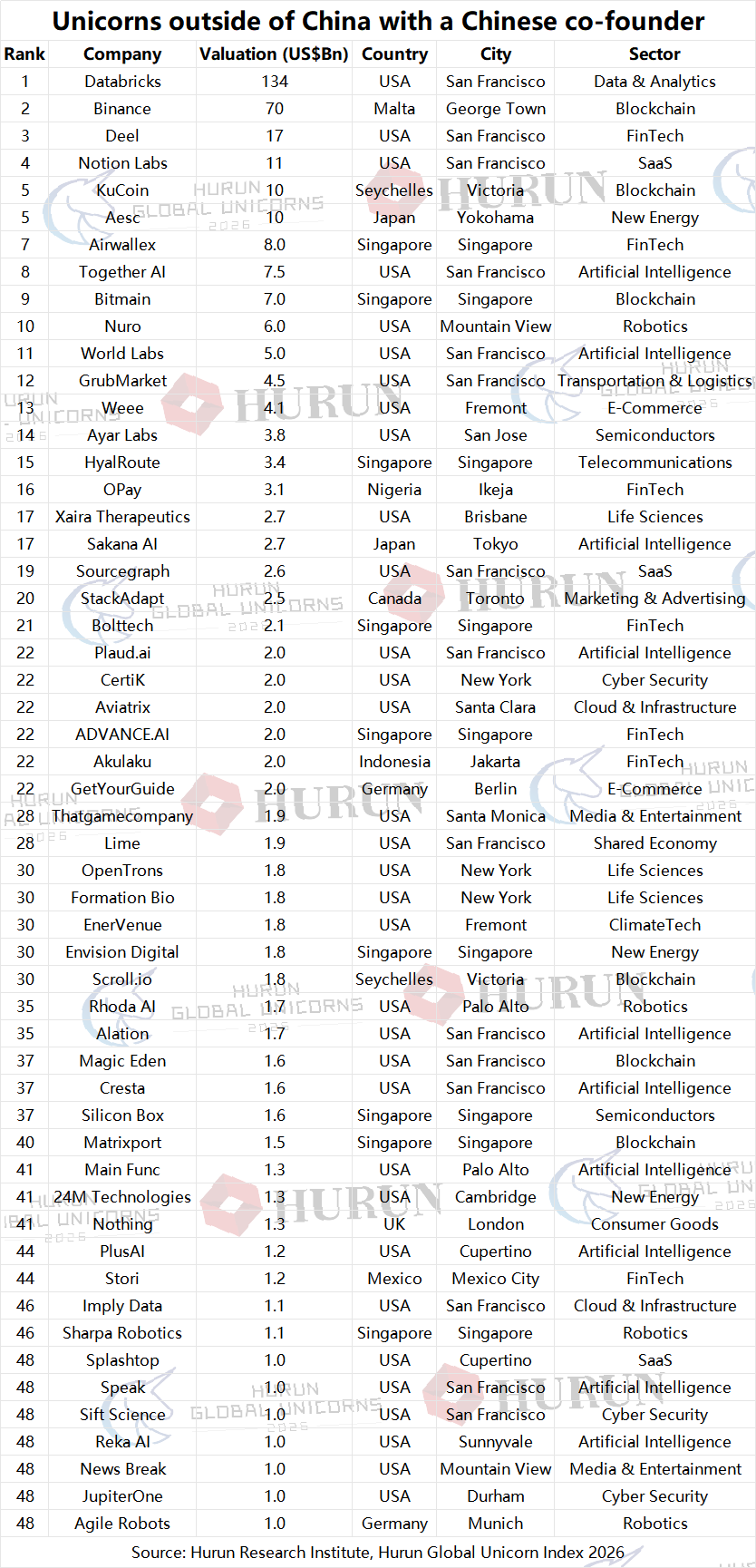

Table: Unicorns outside of China with a Chinese co-founder

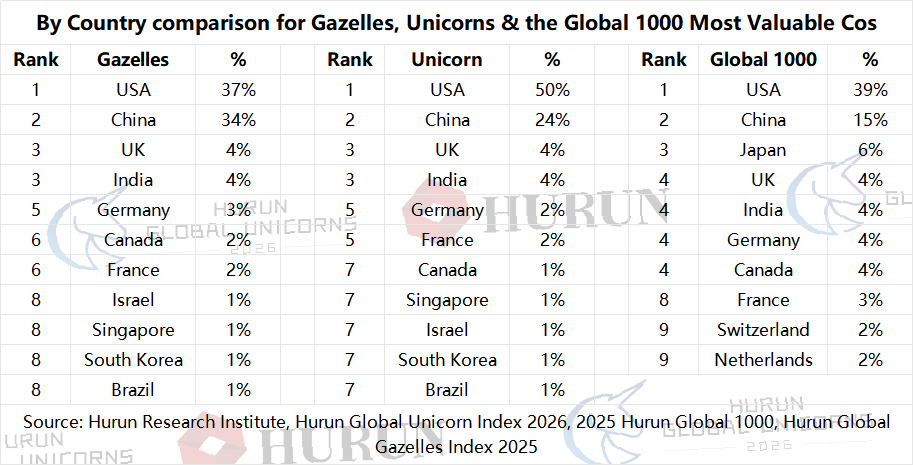

Appendix 4: Comparison between Gazelles, Unicorns, and Global 1000

Gazelles are start-ups founded in the 2000s, not yet listed on a public exchange, and most likely to ‘go unicorn’ within three years. The Hurun Global 1000 is a list of the 1000 most valuable non-state-controlled businesses in the world.

The pipeline for the Hurun Global 1000 is the Global Unicorn Index, the pipeline for the Global Unicorn Index is the Hurun Global Gazelle Index, and the pipeline for the Hurun Global Gazelle Index is the Hurun Global Cheetah Index.

The US, China and India have a higher percentage of Gazelles, and Unicorns, which over the next five years ought to translate into a higher percentage of Hurun Global 1000s. In the same way, Japan, Switzerland and Canada have a small percentage of start-ups, which suggests they will lose ground in the Hurun Global 1000.

By city, San Francisco, New York, Beijing, Shanghai, London, Shenzhen, and Bengaluru have more start-ups and ought to have more Hurun Global 1000s within five years. Tokyo and Paris have fewer startups, so are likely to see their percentage of the world’s most valuable companies go down. London seems to be stable.

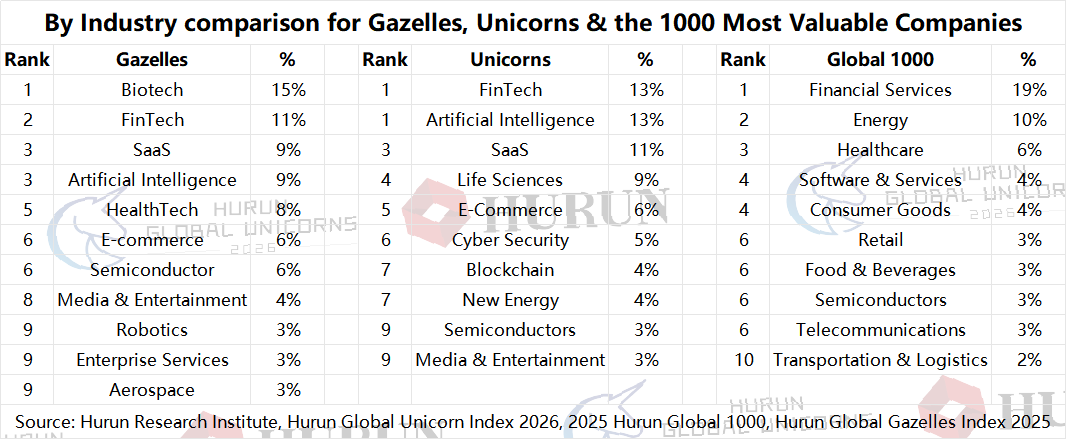

By industry, Financial Services and Software & Services ought to grow into the Hurun Global 1000 companies.

Companies selling B2B and software & services are on the up.

By Country comparison for Gazelles, Unicorns & the Global 1000 Most Valuable Cos

By Industry comparison for Gazelles, Unicorns & the 1000 Most Valuable Companies

Comparison between Cheetahs, Gazelles, Unicorns & the Global 1000 Most Valuable Cos